A Taxing Lesson: Did the End of Section 936 Break Puerto Rico?

- Feb 25

- 16 min read

Updated: Apr 27

John F. McKeon

For three decades, Section 936 of the US Internal Revenue Code served as the linchpin of Puerto Rico’s industrial strategy, reportedly transforming the island into a manufacturing hub by allowing US corporations to repatriate profits nearly tax-free. Section 936 (also known as the Possession Tax Credit) was a provision in our tax code enacted in 1976 ostensibly to encourage business investment in Puerto Rico and other US territories. The provision successfully attracted large corporations in the pharmaceutical and electronics sectors, which at the height of the program's success, accounted for a staggering 42% of the island’s GDP.

Critics argued the incentive primarily functioned as a corporate tax haven that failed to deliver proportional prosperity to the Puerto Rican people, eventually leading Congress to phase out the credit between 1996 and 2006. The subsequent exodus of capital is widely cited as a primary catalyst for the island’s decade-long recession and the spiraling debt crisis that continues to define its modern economic landscape. However, critics and government reports found the credit to be highly inefficient. In 1987, it cost the US Treasury $1.51 in lost revenue for every $1.00 paid in wages to Puerto Rican workers.

Was it a case of profit shifting rather than profit sharing? Corporations often used the provision primarily for tax sheltering rather than local investment. In the chemical industry, average tax benefits per employee were $69,800, while average compensation was only $32,900.

Despite the industrial boom, Puerto Rican per capita income remained less than 30% of the US average, and local unemployment remained more than double the mainland rate.

Long term vulnerability was feared by making investment artificially attractive. The tax credit created an economic bubble. When fully repealed in 2006, Puerto Rico entered a decade-long recession, losing nearly 40% of its manufacturing jobs.

Section 936 allowed US corporations to operate subsidiaries in Puerto Rico (and other US possessions) without paying federal income tax on the profits earned there. While intended to create jobs, it was primarily utilized by capital-intensive industries— specifically pharmaceuticals, electronics, and chemicals to drastically reduce their tax liability through transfer pricing and intellectual property royalties. The most significant beneficiaries were large multinational pharmaceutical and manufacturing companies. (1) The debate over Section 936 remains a central theme in the island's economic history. Below is a breakdown of the primary arguments for and against the provision. Even before a devastating hurricane brought Puerto Rico to a near standstill, the government there was struggling with an economy in shambles and a default on billions of dollars of public debt.

This writer is obligated to ask the following questions: Aside from hurricanes, natural disasters or ‘acts of God’ was all of this economic devastation strictly a result of the changes in the 936 tax incentive? Does that fiscal mess have its roots solely in the repeal of a controversial corporate tax break that helped spark an exodus from the island that sent its economy into reverse? Why and how did the repeal occur? Who was in favor and why? This article will seek to provide information that will permit the reader to decide for themselves.

The Case For and Against Section 936

How Corporations Took Advantage:

Transfer Pricing: Companies would manufacture products in Puerto Rico, but "sell" them to the parent company on the mainland at artificially low prices, or transfer patents to the subsidiary, ensuring high profits were recorded in Puerto Rico (tax-exempt) rather than on the mainland (taxable).

High Profit Margins: Pharmaceutical companies often recorded profits in Puerto Rico that were significantly higher than their mainland operations, with tax breaks sometimes exceeding $70,000 per employee. Aspect Arguments For (The Pros) Arguments Against (The Cons) Econom ic Growth Sparked massive industrialization, transforming Puerto Rico from an agrarian society to a manufacturing hub. Created a "phantom economy" where profits were booked on the island but often flowed back to the mainland. Employ ment Directly created tens of thousands of high-paying jobs in the pharmaceutical and electronics sectors. Critics argued it encouraged capital-intensive industries rather than labor-intensive ones, limiting total job creation. Investm ent Encouraged billions in foreign direct investment and modernized the island's infrastructure. The benefits were seen as a form of corporate welfare that drained the US Treasury of billions in tax revenue. Local Banking Profits held in Puerto Rican banks (936 funds) provided cheap credit for local businesses and mortgages. When the credits were phased out, these funds vanished, contributing to the island's protracted debt crisis.

Investment Income: Companies would invest their tax-free accumulated profits in Puerto Rican financial institutions, which were then loaned back to the companies or the government, adding another layer of tax-exempt income.

The Impact on Puerto Rico produced a concentration of industry whereby the 1990s, Section 936 corporations generated over $10 billion in annual profits and saved roughly $3 billion in taxes. While providing well paying jobs, the industries were ‘capital intensive,' where they employed relatively few people compared to the massive tax breaks they received. The "936" Lobby, a group of about 70 companies, known as the Puerto Rico USA Foundation,(2) heavily lobbied to keep these tax benefits. When the tax code was repealed in 1996, with a 10-year sunset clause, many of these corporations began to shift operations to lower cost countries, contributing to a long-term recession in Puerto Rico.

Core Mechanism and Impact

US subsidiaries in Puerto Rico could repatriate profits to their mainland parent companies nearly tax free, often avoiding both federal and high local taxes.The pharmaceutical and electronics sectors were the primary beneficiaries. At its peak, pharmaceuticals accounted for approximately 50% of the tax credits granted under the program. Section 936 helped transition Puerto Rico from an agricultural economy to an industrial one. At its height, manufacturing represented roughly 42% of Puerto Rico's GDP.

Following years of criticism that the credit was "corporate welfare," Congress initiated a 10-year phase-out in 1996. The final expiration in 2006 coincided with the start of a deep, multi-year recession in Puerto Rico. Manufacturing employment fell sharply in 1995 as many companies relocated to lower-cost foreign jurisdictions. That fiscal mess, partly the result of a prolonged downturn that lingered long after the rest of the US had recovered from the Great Recession, has its roots in the repeal of the controversial corporate tax break that helped spark an exodus from the island and sent its economy into reverse.

In the Beginning

More than half a century ago, US lawmakers sought to help Puerto Rico emerge from its colonial past, transforming its largely agrarian economy into a manufacturing powerhouse. The effort, known as ‘Operation Bootstrap,' began with a series of tax breaks designed to attract manufacturers who would provide steady factory jobs. In the 1950s and 1960s Operation Bootstrap shifted the economy overall from agriculture to industry, Puerto Rico began to offer tax deals to off-Island manufacturers. The idea was to encourage investors. The first law of this kind was passed in 1947 and the number of factories increased. Consumer goods, including apparel, were produced in Puerto Rico in increasing quantities.

For a time the plan seemed to work, as standards of living in Puerto Rico rose. Between 1950 and 1980, per capita gross national product grew nearly tenfold and disposable income and educational attainment also rose sharply according to the Center for a New Economy, a think tank based in San Juan, Puerto Rico. The island experienced rapid industrialization under "Operation Bootstrap," with a 7.3% annual growth rate in net income during this period.

At the end of the 1960s, Puerto Rico made a shift from labor intensive industries like clothing to capital intensive ones like chemical and electronics production. But by the early 1990s, the 936 provision faced growing opposition as a form of corporate welfare. Much like the debate today over corporations parking profits offshore to avoid taxes, tax reformers saw the provision as too costly for the US Treasury. The tax break also had some unintended consequences, notably the unfair tax burden that fell to domestic Puerto Rican companies. Plant closures and job losses followed. Ten years later, on the eve of the 2007 Great Recession, employment in Puerto Rico peaked. Left with a dwindling tax base, the Puerto Rican government borrowed heavily to replace the lost revenue.

Today, the US territory has nearly $70 billion in debt, The unemployment rate in Puerto Rico was approximately 5.4% to 5.6% as of late 2025, This represents a historical low for the island but still remains higher than the US national average (4.1%–4.3%). Yet, only about 40%–42.7% of the working-age population is actually employed. The Island is crippled with insolvent pension systems and a chronically underfunded Medicaid insurance program for the poor. Puerto Rico’s job base continues to shrink, taking its economy along with it. A lack of job prospects has sent many Puerto Ricans fleeing to the mainland, where the job market is much stronger. The out-migration began before the recession sent the US economy into reverse in 2007. From a peak of 3.8 million in 2004, Puerto Rico’s population fell to about 3.2 million last year, according to census estimates, a decline of nearly 11 percent.(3)

The departure of younger workers has left the territory with an older, poorer population, further straining the government’s social services. It’s also left the local economy with fewer active workers.

Just over 40 percent of Puerto Rico’s population was officially counted as part of the labor force. Some of those missing from the workforce are part of an ‘informal economy’ that employs a considerable segment of the population and allows workers and firms to avoid many of the taxes and other costs associated with formal employment.

Puerto Rico does not have "at-will" employment, employers must prove "just cause" for termination or pay statutory severance or ‘mesada’ (4).This rigidity can encourage, in some cases, the hiring of unreported labor to avoid these long-term obligations.

The devastation brought by Hurricane Maria accelerated the migration, as families who have lost their homes sought shelter with relatives on the US mainland. Many see the relocation as temporary, but others may find better opportunities in one of the 50 states, where the average weekly wage is nearly twice that of Puerto Rico.

Profit Shifting over People

Corporations often used the provision primarily for tax sheltering rather than local investment. In the chemical industry, average tax benefits per employee were $69,800, while average compensation was only $32,900. Despite the industrial boom, Puerto Rican per capita income remained less than 30% of the US average, and local unemployment stayed more than double the mainland rate.

Long-term vulnerability arose by making investment "artificially attractive," and the credit created an economic bubble. When it was fully repealed in 2006, Puerto Rico entered a decade-long recession, losing nearly 40% of its manufacturing jobs. In summary, while the average worker in a 936-supported factory earned a better-than-average wage, the broader economy became over-dependent on a tax loophole that primarily enriched multinational corporations and left the island vulnerable to a crash once the incentives vanished

The Beginning of the End

In 1996, President Bill Clinton signed the legislation to phase out Section 936 primarily as part of a broader federal deficit reduction program and to eliminate "corporate welfare". The repeal, which was fully executed by 2006, was driven by several key factors. The Clinton administration sought to raise new revenue to reduce the federal deficit by revoking multibillion-dollar tax breaks for mainland US companies. The Treasury Department viewed Section 936 as an expensive giveaway that allowed large corporations—particularly in the pharmaceutical industry—to avoid billions in taxes without creating proportional local employment or investment. The Clinton administration argued the number of jobs created was too small relative to the high tax expenditure. The administration and Congress determined that companies were "abusing" the law by shifting income earned in the mainland US to Puerto Rican subsidiaries to shield it from taxation.

At the time, Puerto Rico's Statehood Party (PNP),(5) viewed Section 936 as an obstacle to achieving US statehood, unlike the pro-commonwealth party that had long defended it. A legislative compromise arose. In 1996, the Republican-led US Congress added the full phase-out of Section 936 to a bill as a trade that raised the national minimum wage, which was a key policy goal for the Clinton administration.

The phase-out is widely cited by economists as a primary cause of Puerto Rico’s long-term economic decline. As the incentives faded, many US manufacturers closed plants and moved operations to lower-cost locations like China. The final expiration of the provision in 2006 coincided with the start of a deep, multi-year recession in Puerto Rico. To compensate for the shrinking tax base and lost revenue, the Puerto Rican government increased its borrowing, contributing to its eventual $70 billion debt crisis.

‘Repeal and Replace?’

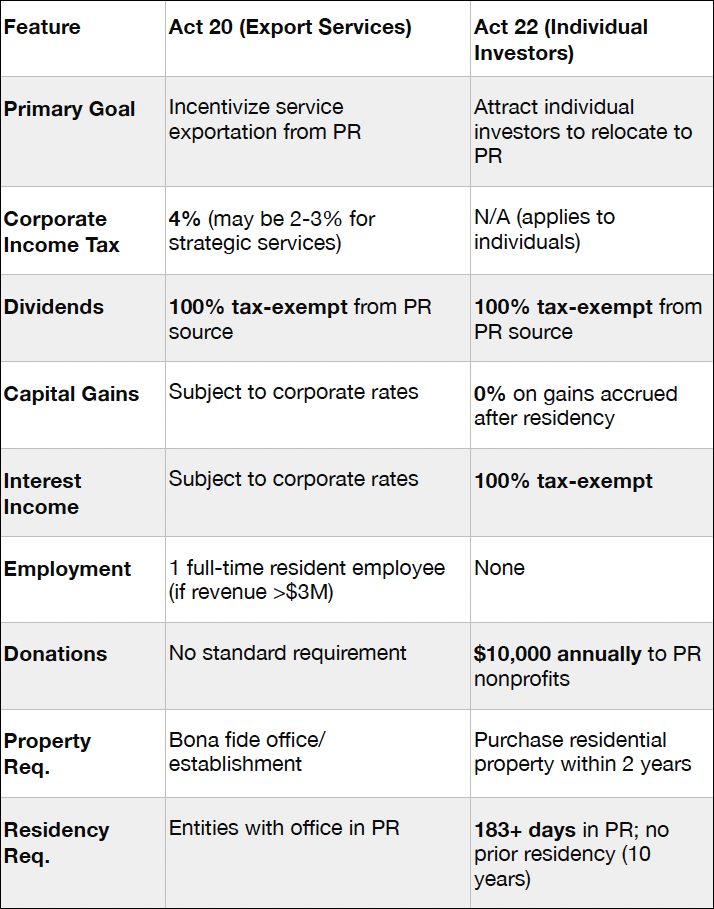

In 2019, Puerto Rico consolidated several older laws (Act 20 and Act 22) into Act 60. Unlike Section 936, which targeted corporate manufacturing, Act 60 largely targets individual wealth and service exports. To remain competitive, Puerto Rico now relies on local incentives like Act 60 (formerly Acts 20 and 22), which offers reduced corporate tax rates as low as 4% for certain export services.

Comparison of Acts 20 and 22 (now under Act 60)

The Key Industries under Act 60 are software development, consulting, legal, and financial services. If you sell a service from Puerto Rico to a client in the US, you pay only a 4% corporate tax rate.

The 0% tax on capital gains for new residents has attracted a wave of crypto investors and hedge fund managers. Substantial credits for the development of hotels and ecotourism projects and significant incentives for local solar and renewable energy manufacturing to solve the island's power grid issues.

The Core Difference for the Worker

Under Section 936 a high-school graduate had a chance to find a stable, middle-class job on a production line. Under Act 60, the benefits for the "average" local worker are more controversial. While Act 60 brings in wealthy residents who spend money in the local economy, critics argue it drives up real estate prices (gentrification) without creating the same volume of stable, high-paying jobs for locals that the old manufacturing plants provided.

In the End

While the repeal of Section 936 is widely regarded as a primary catalyst for Puerto Rico’s economic downturn, it was not the sole cause of the island's financial crisis. The 1996 legislation triggered a significant exodus of manufacturing firms, leading to sharp job losses and a shrinking tax base. However, this "lost decade" was compounded by several other critical factors, including the global Great Recession, massive federal healthcare funding inequities that added billions to the public debt, and especially the restrictive Jones Act, which continues to inflate the cost of imported goods.

A 1984 amendment to the US Bankruptcy Code specifically denied Puerto Rican municipalities the ability to restructure debt under Chapter 9, forcing the government to issue more bonds to pay off old debt and fueling an unsustainable cycle of borrowing. These structural issues, combined with local government mismanagement and the devastating impact of natural disasters like Hurricane María, created a complex web of financial instability that extends far beyond a single tax policy

Puerto Rico has also made its share of mistakes. The island’s government never fully dealt with its own finances, lacking modern systems to control and monitor spending. It entered into shortsighted tax agreements with multinational corporations that sacrificed long-term revenue in order to address short-term budget shortfalls. It cut public investment as the economy shrank, weakening the island’s infrastructure, and never dealt with critical initiatives, such as modernizing Puerto Rico’s outdated electrical grid.

However, the US government also bears a great deal of responsibility for the island’s plight. When federal policies that aided Puerto Rico’s economic development were repealed, no enduring replacements were put in place. Washington largely ignored Puerto Rico until it was clear that the island was in severe financial distress and would default on its debt without the protections granted to US municipalities when they file for bankruptcy.

In 2016 Congress passed legislation to create a process akin to bankruptcy that would allow the island’s debt to be restructured in court. It also established an oversight board responsible for supervising the island’s finances and ensuring that it would eventually regain access to credit markets. Necessary to gain bipartisan support for the bill, the creation of the board—with seven members appointed was part of the deal and was a reminder of the island’s colonial status.Yet Congress still did nothing to address Puerto Rico’s incomplete integration into the federal safety net, leaving the island’s residents more exposed to poverty than US citizens on the mainland.

Residents are generally ineligible for the federal Earned Income Tax Credit (EITC) and have limited access to the Child Tax Credit which supplements the income of poor Americans. And although Puerto Rico participates to varying degrees in other federal safety net programs, including Medicaid and Medicare, a 2014 study by the Government Accountability Office estimated that Puerto Rico received less in annual federal benefits than continental US citizens. (6)

Should Puerto Rican families receive EITC benefits when filing federal income taxes? (7) Well… access to the EITC would not only help to alleviate poverty but would also add incentives for lower-income individuals to work. Yet even after the repeal of Section 936, firms operating in Puerto Rico can still avoid US corporate income tax, paying the much lower “global minimum” rate applied to foreign intangible income.

It is critical to note that income was not distributed proportionally through higher wages and better employment opportunities. Therefore it is difficult to discern the actual success of the 936 exemption.(8) The Senate Finance Committee prepared a report after the end of 936 which concluded simply: “Section 936 of the Internal Revenue Code was not an effective means to promote economic growth in Puerto Rico, and the emergence of the current and long-continuing recession cannot be attributed to the termination of 936.”

Some manufacturers left Puerto Rico once their sleight of hand no longer produced unreasonable surpluses. However, many stayed and more have invested in the Island since then. Puerto Rico has good reason to be proud of its pharmaceuticals industry. Puerto Rico is the largest exporter of medical supplies in the United States. The next in line are California and Indiana, Puerto Rico produces more than the two states combined. This covers 30% of Puerto Rico’s total manufacturing output and employs 90,000 people. These workers average 60% higher wages than the average manufacturing job on the Island. Have Congressional actions shaped Puerto Rico’s economic trajectory? How did we get to this moment? We need to review the past

Congressional Acts with Major Economic Impact on Puerto Rico

It all began with an important 1901 US Supreme Court ruling known as Downes v. Bidwell, 182 US 244 (1901), was a landmark 5-4 Supreme Court decision holding that the US. Constitution does not automatically apply to all territories under American control. Ruling on the Foraker Act,(9) the Court determined that Puerto Rico was an "unincorporated territory" belonging to, but not part of, the US and described Puerto Rico as “belonging to the United States, but not a part of the United States,”(10) This was the first of many questionable US government actions that directly affected the economic life of the territories. The present financial status is a result of fiscal mismanagement, relatively high labor costs, and the loss of federal tax subsidies. Meanwhile, the population has declined because of massive emigration.

Congressional Acts

Key Ongoing Factors

Statutory caps on Medicaid funding and exclusion from certain low-income tax credits (like the full Earned Income Tax Credit) have historically limited Puerto Rico's social safety net compared to US states.

In December 2015, President Barack Obama’s administration called on Congress to adopt a blueprint that proposed allowing Puerto Rico to restructure its debt, strengthen financial oversight, expand Medicaid and give residents access to the same low-income tax credits available to other American citizens. In 2016, under the Obama Administration the US Congress enacted the Puerto Rico Oversight, Management, and Economic Stability Act to deal with the island’s severe debt crisis. Although it promised financial relief, the legislation was a blow to the island’s sovereignty.

Federal debt restructuring processes under PROMESA have faced criticism for potentially leading to significant electric rate hikes (up to 34%) to pay bondholders.

In early 2025, executive freezes on certain federal funds and potential new tariffs on imported goods have created fresh uncertainty for the island's manufacturing and consumer costs

Economic Impact of Limited Sovereignty (2026 Data)

Economists project that by 2026, the island's margin between "modest growth and missed opportunity" will be narrow as federal recovery funds decrease and the structural costs of its territorial status—such as the 4 times higher shipping costs under the Jones Act remain in place.

In conclusion, while the repeal of Section 936 was a significant turning point, it was merely one catalyst in a complex web of structural and systemic failures that dismantled the Puerto Rican economy. Ultimately, Puerto Rico’s economic destruction resulted from an inherent state of constant crisis born of its unique territorial status—a position that leaves it subject to federal mandates like the Jones Act while denying it the sovereign tools or state-level protections needed to recover. The future of Puerto Rico is a Ineligible for Bankruptcy Restricted Debt Relief Unlike US states, Puerto Rico cannot use standard municipal bankruptcy law (Chapter 9), leading to protracted and costly debt restructuring under unique federal mandates. Federal Tax Policy Shifts Industrial Instability The repeal of historical federal tax provisions (like Section 936) contributed to a long-term loss of manufacturing and tax base. question of ideology and identity, and both are critical steps in allowing Puerto Rico to chart a sustainable long-term economic course. As for the US, which has ruled Puerto Rico as a colony for well over a century, giving the people of Puerto Rico the chance to have more of a say in their own future is not only a good policy and a good decision— it’s time has come.

Historian John F. McKeon lives on St. Croix USVI and in Southampton NY. He holds degrees from Trinity College Dublin, (MPhil with Distinction). and St. Joseph's University New York (Summa Cum Laude) B.A. East Asian History with a Philosophy Capstone Minor in Labor, Class and Ethics. John also has certificate from the Oxford University Epigeum Research Integrity Center. He is a current member of the Society of Virgin Island Historians.

Sources:

A Credit for All Reasons: The Ambivalent Role of Section 936 Ann J. Davidson The University of Miami Inter-American Law Review , Fall, 1987, Vol. 19, No. 1 (Fall, 1987), pp. 97-136

How Congress shaped Puerto Rico’s status — and its struggle for equality

Paul Carrillo & Anthony Yezer & Jozefina Kalaj, 2017. Could Austerity Collapse the Economy of Puerto Rico? 2017, The George Washington University, Institute for International Economic Policy.

Web:

Foot Notes:

Pharmaceutical Companies: Johnson & Johnson,Pfizer,Merck,Abbott Laboratories,Bristol Myers Squibb,Eli Lilly,Baxter International, Schering-Plough,Warner-Lambert, American Home Products, Roche

Other Manufacturers and Corporations: Coca-Cola (noted for high tax savings per employee), PepsiCo, Digital Equipment Corporation, Procter & Gamble (implied via manufacturing presence), Motorola, General Electric and Revlon

This organization is a policy-oriented group based in Washington, DC, focused on the political and legal relationship between Puerto Rico and the United States. The foundation has historically petitioned the US Congress to grant Puerto Rico "incorporated territory" status as a step toward permanent union and statehood. It has advocated for programs like Empowerment Zones to generate economic expansion and attract research-oriented businesses to the island.

The current population of Puerto Rico is estimated to be approximately 3.2 million (roughly 3,184,835 to 3,230,958) as of early 2026, according to recent data from the US Census Bureau the population has been steadily declining due to low fertility and migration to the US mainland, experiencing a 0.6% decline between 2024 and 2025

In Puerto Rico, mesada typically means a monthly payment, allowance, or stipend. While in many Latin American regions it can refer to a kitchen countertop, in the context of money, it translates directly to a regular allowance or, in some contexts, a monthly salary.

In Puerto Rico, PNP refers to the New Progressive Party (Partido Nuevo Progresista), one of the island's two dominant political organizations. Its core mission is advocating for Puerto Rico to become the 51st US State.

https://www.volckeralliance.org/sites/default/files/attachments/America's Forgotten Colony - Foreign Affairs.pdf

Residents must file a federal return if they work for the federal government, are in the US military, or have income from sources outside of Puerto Rico.Residents pay federal Social Security and Medicare taxes, similar to citizens in the 50 states. Despite the exemption on local income, Puerto Rico residents paid over $5 billion in federal taxes in 2023, largely through payroll and excise taxes. Puerto Rico has its own tax system with high, progressive tax rates, often higher than those in the US states.

For example; Microsoft copied software onto discs in Puerto Rico and claimed all the profits for that software were produced in Puerto Rico — but actually had fewer than 200 workers on the Island https://puertoricoreport.com/economics-laureate-joseph-stiglitz-on-the-causes-of-puerto-ricosfinancial-crisis/

Signed into law by President McKinley on April 12, 1900, the Foraker Act (or Organic Act of 1900) established a civilian government in Puerto Rico, replacing U.S. military rule after the Spanish-American War. It designated the island as an unorganized territory, created a governor and executive council appointed by the US President, and allowed for an elected House of Delegates, while imposing tariffs on goods.

In 1901, the US Supreme Court decided the "Insular Cases," a series of rulings—most notably Downes v. Bidwell—establishing that Puerto Rico is an unincorporated territory belonging to, but not part of, the United States. The Court ruled the Constitution does not fully apply to these territories.